Deal To Watch: Who Needs College

Key Stats:

| Valuation Cap |

Amount Raised

N/A |

Number of Investors

N/A |

|

Minimum Raise

N/A |

Maximum Raise

N/A |

Likelihood of Max

N/A |

|

Start Date

N/A |

Stop Date

N/A |

Days Remaining

|

|

Security Type

N/A |

Investment Minimum

$N/A |

Deal Analytics |

Summary

To date and as of 6/6, Eazl has raised $39,900

The Eazl team has been selected as a “Deal To Watch” by KingsCrowd. This distinction is reserved for deals selected into the top 10-20% of our due diligence funnel. If you have questions regarding our deal diligence and selection methodology please reach out to hello@kingscrowd.com.

Problem

One of America’s most pressing problems is the growing debt arising from college tuition. U.S students currently hold roughly more than $1.56 trillion in college debt. On top of this, college degrees, especially online degrees, are becoming less significant as higher percentages of job applicants have the same or similar credentials.

An incredible 47% of college students in a Gallup poll even remarked that they do not think their education adequately prepared them for a successful career. These facts are even beginning to resonate with major firms such as Google, Apple, and 15 other Fortune 500 companies – all of which no longer require a college degree in order to apply for employment.

The time has come to replace the necessity of a college degree.

Wall Street has Morningstar, S&P, and Bloomberg

The equity crowdfunding market has KingsCrowd.

Solution

In order to combat each of these issues, Eazl has come up with a new way of offering online education. Rather than simply offering quality courseware, Eazl enables its students access to one-on-one mentorship and challenges that are more relevant to problems the students will encounter in the real world.

When the students pass these challenges, they receive skill badges. These badges, that can be verified by employers or clients, prove that the student learned the skill. In turn, it enables students to differentiate themselves among their peers. Afterwards, the student receives feedback on their work from a programmed mentor. Badges can be advertised on resumes and LinkedIn Profiles.

Eazl ensures this model results in a cheaper way for students to receive their education by providing the courseware for free and having students pay for the special challenges with Eazl coins.

According to Eazl, it amounts to over $35,000 in savings compared to a traditional college and can be completed in 1/10th of the time.

Product Background

Eazl was founded in 2013 in response to the founders’ frustration at the college process and the debt that comes with it.

The online course they installed, known as “Career Hacking”, took off. Due to the success of Career Hacking, Eazl was asked to make courses for popular topics by Udemy, the world’s leading distributor of online courses for over 200,000 students in 193 countries.

Additionally, Eazl began to work with Picture Show Films, an Emmy Award Winning Production Company, to create video-based learning experiences for students. Some of these videos became best-selling courses on Udemy.com.

Why We Like it

1. Market Size

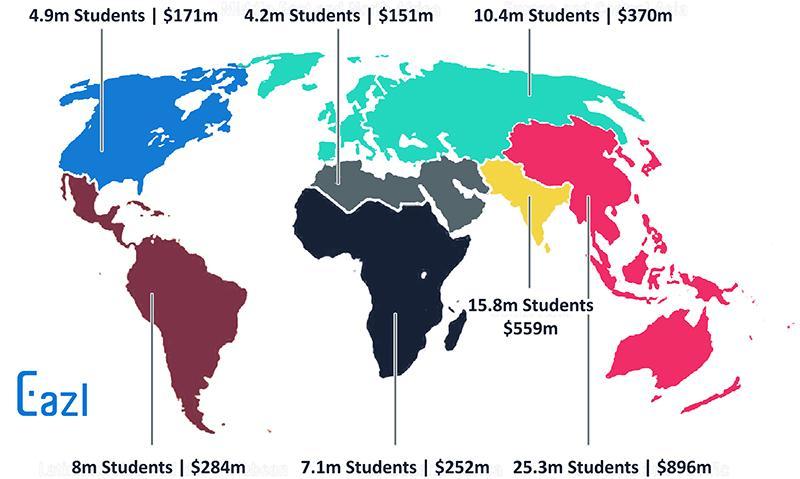

Eazl can already be considered a global business school not only due to its popularity among Udemy.com users but also due to the fact that the global market for career readiness programs is projected at $2.7 billion and including 76 million students.

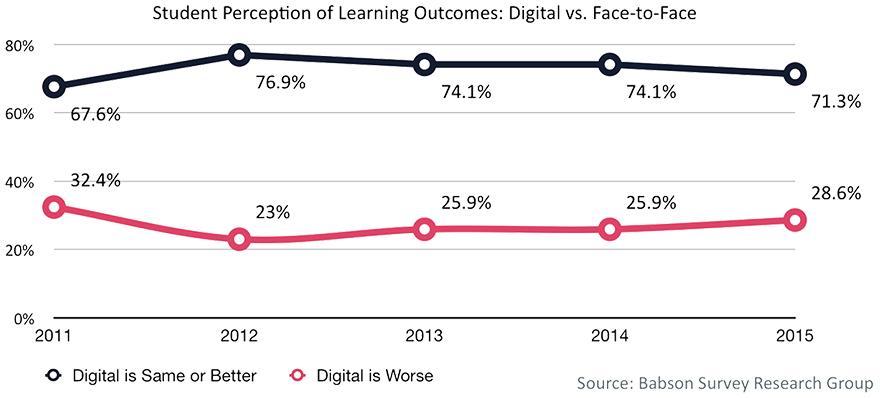

This is thanks, in part, to the fact that more and more students prefer digital learning: According to the Babson Survey Research Group, roughly 71% of students perceive digital learning to be the same or better in comparison to face-to-face learning.

Eazl is already providing courseware for over 200,000 students in 193 different countries through Udemy.com. As a result, major companies such as Tesla, Apple, The World Bank, PayPal, and Lyft have adopted Eazl’s courseware. Even Harvard University is climbing abord.

2. Product Differentiation

Currently, there are very few, if any, online education offerings that are able to provide easily verifiable forms of confirmation for skill completion. Additionally, in the world of online education, many students miss out on personalized feedback that face-to-face learning enables. However, with Eazl’s interactive courseware, students can receive one-to-one mentorship feedback on the challenges they complete.

Moreover, the fact that Eazl has already established itself in the online education industry through its Career Hacking course helps separate itself from competitors.

3. Potential Risks

One of the main risks concerning Eazl’s product offering is the long-term viability of its business model. More specifically, many of the students who register for their courseware will be tempted to simply utilize the free aspects of the service rather than paying for additional challenges. Since Eazl’s revenue is dependent upon students purchasing this service, it may struggle to generate significant revenues in the future.

Furthermore, Eazl is operating in a highly competitive market with many online education providers and deep-pocketed skills-based academies such as General Assembly, which provide drastically more affordable programs for learning skills and getting jobs at a fraction of college tuition cost. However, most of these programs are focused specifically on computer science and most involve an in-person component.

Wall Street has Morningstar, S&P, and Bloomberg

The equity crowdfunding market has KingsCrowd.

Rating

The Rating: Deal To Watch

Eazl is a Deal To Watch. Eazl is striving to fix a complicated issue for many Americans struggling to not only differentiate themselves in their job applications but also to pay off their student loan debt. However, through their combined usage of quality courseware with paid challenges for verifiable badges, Eazl is offering a legitimate alternative to costly traditional colleges.

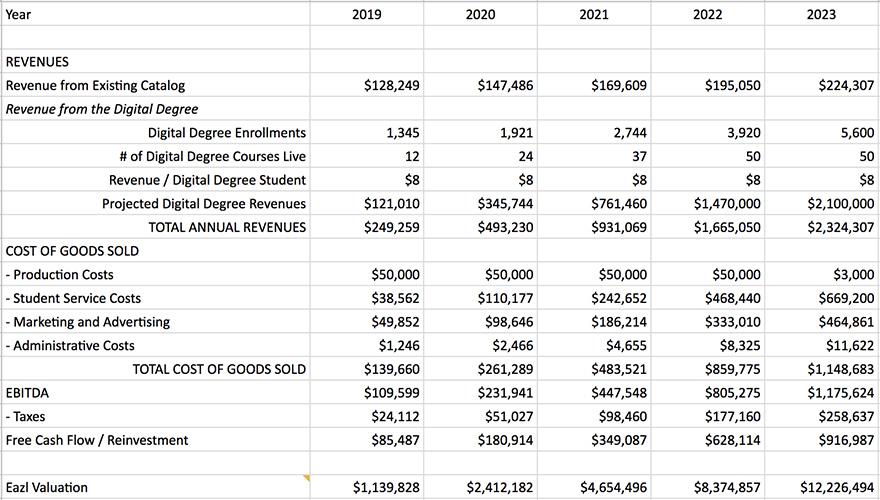

Its financial projections appear both reasonable and speak for themselves:

Source: Eazl via Trucrowd.

In spite of the capital resources available to their competitors, the size of the market can provide room for Eazl to carve out a sizeable niche that can still provide nice returns from the current $3.2M valuation.

This does not seem to be a rocket ship type investment and the reality is, despite significant success in getting major partnerships like the one with Udemy to have distribution access to hundreds of thousands of students, revenues have not followed. It appears as though content licensing fees are relatively low, and growth will largely have to come from students that enroll for the digital degree program, which is unproven at this point.

It does seem as though the team has built a quality product and has managed to remain lean while revenues have remained limited. With team expectations of a $12M valuation in the next 5 years this won’t be a huge win. However, it feels as though some of the downside risk of the business has been minimized because of their relationship with Udemy.

We can see a world where Udemy acquires Eazl to grow their portfolio of content. And should Eazl actually continue to grow the valuation may even be more frothy in this event. Time will tell on this one, as they need to prove out traction with their digital degree enrollments.

With a strong product offering in an on-trend/growing market, but a limited upside in the next 3 to 5 years, this is a Deal To Watch for investors.